|

|

June 26th, 2018

If ever it could be said that there is such a thing as miracle healing soil, Ivan Sanderson said it best in his 1965 book entitled Ivan Sanderson’s Book of Great Jungles.

King Leopold’s Soliloquy

Sanderson grew up with a natural inclination towards adventure and learning. He hailed from Scotland but spent much of his youth in Provence, France where he moved with his parents as a young boy. His description of Provence painted with his youthful imagination would later lead to a lifetime of jungle adventure across all points on the map. Sanderson’s father was killed by a rhinoceros while working with a documentary film crew in Kenya, Africa in 1925. Continue reading Antibiotic Properties of Jungle Soil

June 26th, 2018

Toxicity of Rhododendron

From Countrysideinfo.co.UK

“Potentially toxic chemicals, particularly ‘free’ phenols, and diterpenes, occur in significant quantities in the tissues of plants of Rhododendron species. Diterpenes, known as grayanotoxins, occur in the leaves, flowers and nectar of Rhododendrons. These differ from species to species. Not all species produce them, although Rhododendron ponticum does. Continue reading Herbal Psychedelics – Rhododendron ponticum and Mad Honey Disease

June 26th, 2018

For years in the West African nation of Ghana medicine men have used a root and leaves from a plant called nibima(Cryptolepis sanguinolenta) to kill the Plasmodium parasite transmitted through a female mosquito’s bite that is the root cause of malaria. A thousand miles away in India, a similar(same) plant with similar properties called maranta, or Cryptolepis buchananii (Indian sarsaparilla), is used by Ayurvedic doctors to treat an assortment of ailments from urinary tract infection to paralysis and ricketts. Continue reading Curing Diabetes With an Old Malaria Formula

June 24th, 2018

By the time I got to California the blondes had gone home

The Beach Boys were sporting dreadlocks

and singing reggae songs

The life guard at the tower

didn’t have a tan

Said if you’re looking for Mama Cass

she’s asleep over there in the van Continue reading The Last Surfer in California

June 24th, 2018

Every home should have one to be opened in spring

A jar that sits on the table full of baseball dreams

Inside will be found there pennants and things

The smell of fresh cut grass and pinstriped rings

A pair of old tickets to the game never played,

Do you remember how cold it was on that day? Continue reading A Jar of Baseball Dreams

June 15th, 2018  Anthonie van Leeuwenhoek 1680-1686 For one suffering gout, the following vitamins, herbs, and extracts may be worth looking into:

- Vitamin C

- Folic Acid – Folic Acid is a B vitamin and is also known as B9 – [Known food sources with high contents of folic acid include dark leafy green vegetables such as avocados, seaweed, spinach, asparagus and brussel sprouts. Liver, yeast, eggs, legumes, seafood and nuts are also a good source.

- Eicosapentaenoic acid or EPA – [Known food sources include oily fish such as herring, mackerel, salmon, sardines and seaweed. The EPA in fish comes for the algae that fish consume.

- Black Cherry Extract

- Celery Seed Extract

- Alfalfa

- Bosweilla – Anti-inflammatory properties

- Devils Claw – Anti-inflammatory properties

- Turmeric & Curcumin – [Studies have shown positive effects for rheumatoid arthritis and general pain and inflammation. Curcumin has also been shown to block the growth of certain kinds of tumors. Positive effects have noted on diabetes and viral infections.]

CAUTION: As with any herbs, extracts, supplements, and vitamins, one should check with their doctor prior to taking to ensure there will not be negative interactions with prescription medications one might be taking.

Many herbs and vitamins have side effects. Side effects for most herbs, extract, supplements, and vitamins can be found on WebMD.com.

June 15th, 2018

Buying a book for a serious collector with refined tastes can be a daunting task.

However, there is one company that publishes some of the finest reproduction books in the world, books that most collectors wouldn’t mind having in their collection no matter their general preference or specialty. Continue reading Looking for a Gift for the Book Collector in the Family?

May 9th, 2018

Notes on the intaglio processes of the most expensive book on birds available for sale in the world today.

The Audubon prints in “The Birds of America” were all made from copper plates utilizing four of the so called “intaglio” processes, engraving, etching, aquatint, and drypoint. Intaglio processes are those by which the design to printed is cut down into the surface of the plate, and will yield an impression in relief.

The design is rendered upon the plate either with a tool or by the action of an acid eating into the copper plate through an acid resistant coating called a “ground.” Continue reading The Intaglio Processes for Audubon’s Birds of America

May 9th, 2018  Wild Turkeys by John James Audubon Audubon started to develop a special technique for drawing birds in 1806 a Miill Grove, Pennsylvania. He perfected it during the long river trip from Cincinnati to New Orleans and in New Orleans, 1821. Continue reading Audubon’s Art Method and Techniques

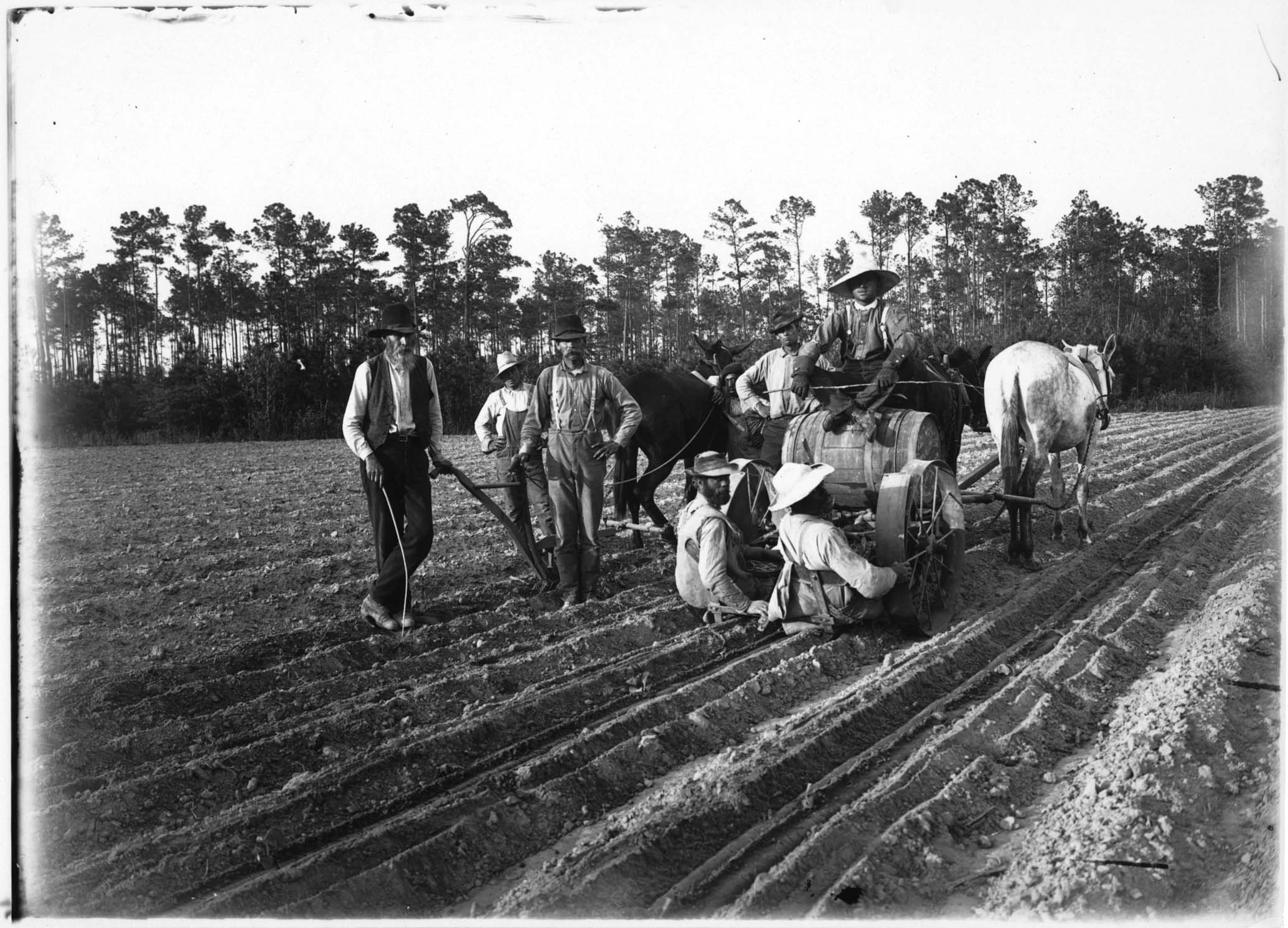

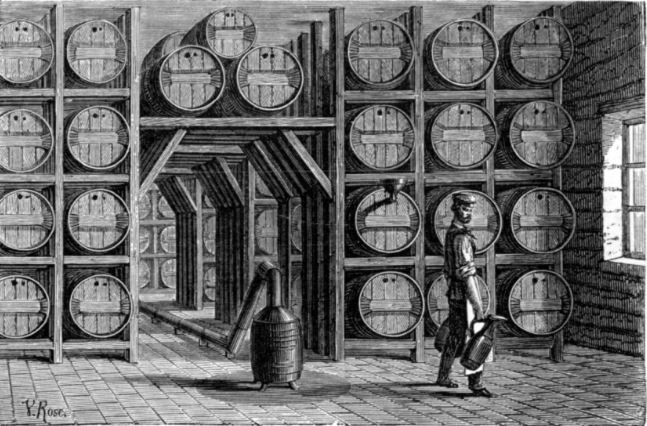

May 6th, 2018  Chipping a Turpentine Tree DISTILLING TURPENTINE

One of the Most Important Industries of the State of Georgia

Injuring the Magnificent Trees

Spirits, Resin, Tar, Pitch, and Crude Turpentine all from the Long Leaved Pine – “Naval Stores” So Called.

Dublin, Ga., May 8. – One of the most important industries of Georgia is the distilling of turpentine. Here and there among the thick tracts of yellow pines, so numerous in South Georgia, can be found many turpentine farms, more properly called stills, which are fast sapping away the life of the magnificent timber in that section. A visit to one of these stills is well worth the time. Continue reading Naval Stores – Distilling Turpentine

May 4th, 2018

ON

THE ORIGIN OF SPECIES

BY MEANS OF NATURAL SELECTION,

OR THE

PRESERVATION OF FAVOURED RACES IN THE STRUGGLE

FOR LIFE.

BY CHARLES DARWIN, M.A.,

FELLOW OF THE ROYAL, GEOLOGICAL, LINNÆAN, ETC., SOCIETIES ;

AUTHOR OF ‘JOURNAL OF RESEARCHES DURING H.M.S. BEAGLE’S VOYAGE

ROUND THE WORLD.’

LONDON: JOHN MURRAY, ALBEMARLE STREET.

1859.

LONDON: PRINTED BY W. CLOWES AND SONS, STAMFORD STREET,

AND CHARING CROSS.

ON THE ORIGIN OF SPECIES.

INTRODUCTION.

WHEN on board H.M.S. ‘Beagle,’ as naturalist, I was much struck with certain facts in the distribution of the inhabitants of South America, and in the geological relations of the present to the past inhabitants of that continent. These facts seemed to me to throw some light on the origin of species—that mystery of mysteries, as it has been called by one of our greatest philosophers. On my return home, it occurred to me, in 1837, that something might perhaps be made out on this question by patiently accumulating and reflecting on all sorts of facts which could possibly have any bearing on it. After five years’ work I allowed myself to speculate on the subject, and drew up some short notes; these I enlarged in 1844 into a sketch of the conclusions, which then seemed to me probable: from that period to the present day I have steadily pursued the same object. I hope that I may be excused for entering on these personal details, as I give them to show that I have not been hasty in coming to a decision. Continue reading On the Origin of Species – Natural Selection by Charles Darwin

May 3rd, 2018

Here, where these low lush meadows lie,

We wandered in the summer weather,

When earth and air and arching sky,

Blazed grandly, goldenly together.

And oft, in that same summertime,

We sought and roamed these self-same meadows,

When evening brought the curfew chime,

And peopled field and fold with shadows.

I mind me of our last fond tryst:

The night was such a night as this:

And standing here, breast-high in mist,

We sealed our parting vows with kisses.

Ah, trust misplaced! ah, last false kiss!

She with another mate tomorrow;

And now my uttermost of bliss

Is made my uttermost sorrow.

I wrestle sore in bitter strife,

For night draws round me dull and darkling,

And in my darkened sky of life

No single star of hope is sparkling

Anonymous – Published in Harper’s Weekly Oct. 4, 1873

May 3rd, 2018

CLAIRVOYANCE AND OCCULT POWERS

By Swami Panchadasi

Copyright, 1916

By Advanced Thought Pub. Co. Chicago, Il

INTRODUCTION.

In preparing this series of lessons for students of Western lands, I have been compelled to proceed along lines exactly opposite to those which I would have chosen had these lessons been for students in India. This is because of the diametrically opposite mental attitudes of the students of these two several lands.

The student in India expects the teacher to state positively the principles involved, and the methods whereby these principles may be manifested, together with frequent illustrations (generally in the nature of fables or parables), serving to link the new knowledge to some already known thing. The Hindu student never expects or demands anything in the nature of “proof” of the teachers statements of principle or method; in fact, he would regard it as an insult to the teacher to ask for the same. Consequently, he does not look for, or ask, specific instances or illustrations in the nature of scientific evidence or proof of the principles taught. Continue reading Clairvoyance and Occult Powers

May 3rd, 2018

CLAIRVOYANCE

by C. W. Leadbeater

Adyar, Madras, India: Theosophical Pub. House

[1899]

CHAPTER IX – METHODS OF DEVELOPMENT

When a men becomes convinced of the reality of the valuable power of clairvoyance, his first question usually is, “How can I develop in my own case this faculty which is said to be latent in everyone?”

Now the fact is that there are many methods by which it may be developed, but only one which be at all safely recommended for general use—that of which we shall speak last of all. Among the less advanced nations of the world the clairvoyant state has been produced in various objectionable ways; among some of the non-Aryan tribes of India, but the use of intoxicating drugs or the inhaling of stupefying fumes; among the dervishes, by whirling in a mad dance of religious fervour until vertigo and insensibility supervene; among the followers of the abominable practice of the Voodoo cult, by frightful sacrifices and loathsome rites of black magic. Continue reading Clairvoyance – Methods of Development

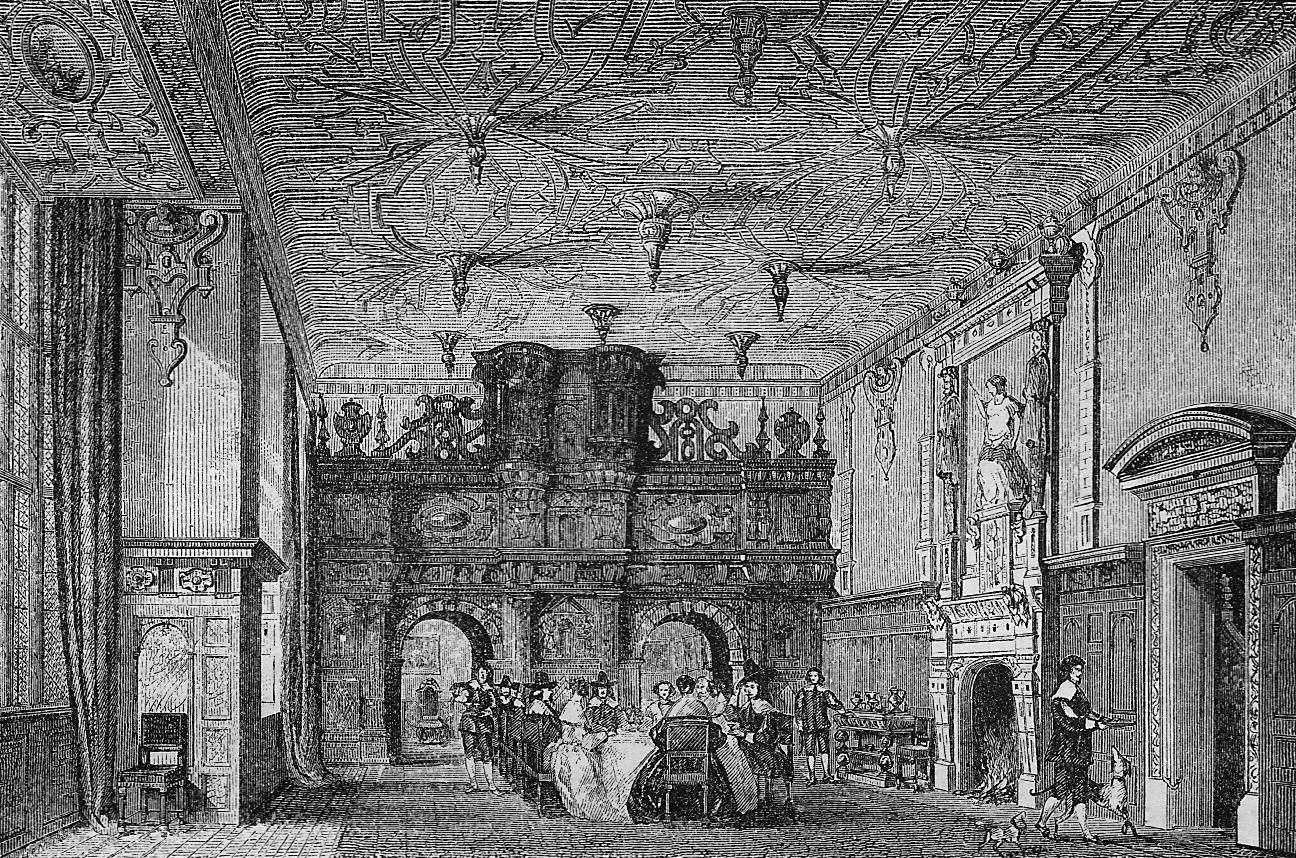

April 27th, 2018  Noel Desenfans and Sir Francis Bourgeois, circa 1805 by Paul Sandby, watercolour on paper The Dulwich Picture Gallery was England’s first purpose-built art gallery and considered by some to be England’s first national gallery. Founded by the bequest of Sir Peter Francis Bourgois, dandy, the gallery was built to display his vast picture collection and dedicated to public viewing, something that had not been done before in Great Britain as art collecting was considered a folly of toffs. Continue reading Sir Peter Francis Bourgeois and the Dulwich Picture Gallery

February 24th, 2026  Tulipmania This transcript is a work in progress…

MEMOIRS OF EXTRAORDINARY POPULAR DELUSIONS AND THE MADNESS OF CROWDS.

By CHARLES MACKAY, LL.D.

CONTENTS.

-

John Law; his birth and youthful career—Duel between Law and Wilson—Law’s escape from the King’s Bench—The “Land-bank”—Law’s gambling propensities on the continent, and acquaintance with the Duke of Orleans—State of France after the reign of Louis XIV.—Paper money instituted in that country by Law—Enthusiasm of the French people at the Mississippi Scheme—Marshal Villars—Stratagems employed and bribes given for an interview with Law—Great fluctuations in Mississippi stock—Dreadful murders—Law created comptroller-general of finances—Great sale for all kinds of ornaments in Paris—Financial difficulties commence—Men sent out to work the mines on the Mississippi, as a blind—Payment stopped at the bank—Law dismissed from the ministry—Payments made in specie—Law and the Regent satirised in song—Dreadful crisis of the Mississippi Scheme—Law, almost a ruined man, flies to Venice—Death of the Regent—Law obliged to resort again to gambling—His death at Venice

-

Originated by Harley Earl of Oxford—Exchange Alley a scene of great excitement—Mr. Walpole—Sir John Blunt—Great demand for shares—Innumerable “Bubbles”—List of nefarious projects and bubbles—Great rise in South-sea stock—Sudden fall—General meeting of the directors—Fearful climax of the South-sea expedition—Its effects on society—Uproar in the House of Commons—Escape of Knight—Apprehension of Sir John Blunt—Recapture of Knight at Tirlemont—His second escape—Persons connected with the scheme examined—Their respective punishments—Concluding remarks

-

Conrad Gesner—Tulips brought from Vienna to England—Rage for the tulip among the Dutch—Its great value—Curious anecdote of a sailor and a tulip—Regular marts for tulips—Tulips employed as a means of speculation—Great depreciation in their value—End of the mania

-

Introductory remarks—Pretended antiquity of the art—Geber—Alfarabi—Avicenna—Albertus Magnus—Thomas Aquinas—Artephius—Alain de Lisle—Arnold de Villeneuve—Pietro d’Apone—Raymond Lulli—Roger Bacon—Pope John XXII.—Jean de Meung—Nicholas Flamel—George Ripley—Basil Valentine—Bernard of Trèves—Trithemius—The Maréchal de Rays—Jacques Cœur—Inferior adepts—Progress of the infatuation during the sixteenth and seventeenth centuries—Augurello—Cornelius Agrippa—Paracelsus—George Agricola—Denys Zachaire—Dr. Dee and Edward Kelly—The Cosmopolite—Sendivogius—The Rosicrucians—Michael Mayer—Robert Fludd—Jacob Böhmen—John Heydon—Joseph Francis Borri—Alchymical writers of the seventeenth century—Delisle—Albert Aluys—Count de St. Germain—Cagliostro—Present state of the science

-

Terror of the approaching day of judgment—A comet the signal of that day—The prophecy of Whiston—The people of Leeds greatly alarmed at that event—The plague in Milan—Fortune-tellers and Astrologers—Prophecy concerning the overflow of the Thames—Mother Shipton—Merlin—Heywood—Peter of Pontefract—Robert Nixon—Almanac-makers

-

Presumption and weakness of man—Union of Fortune-tellers and Alchymists—Judicial astrology encouraged in England from the time of Elizabeth to William and Mary—Lilly the astrologer consulted by the House of Commons as to the cause of the Fire of London—Encouragement of the art in France and Germany—Nostradamus—Basil of Florence—Antiochus Tibertus—Kepler—Necromancy—Roger Bacon, Albertus Magnus, Arnold Villeneuve—Geomancy—Augury—Divination: list of various species of divination—Oneiro-criticism (interpretation of dreams)—Omens

-

The influence of imagination in curing diseases—Mineral magnetisers—Paracelsus—Kircher the Jesuit—Sebastian Wirdig—William Maxwell—The Convulsionaries of St. Medard—Father Hell—Mesmer, the founder of Animal Magnetism—D’Eslon, his disciple—M. de Puysegur—Dr. Mainauduc’s success in London—Holloway, Loutherbourg, Mary Pratt, &c.—Perkins’s “Metallic Tractors”—Decline of the science

-

Early modes of wearing the hair and beard—Excommunication and outlawry decreed against curls—Louis VII.’s submission thereto the cause of the long wars between England and France—Charles V. of Spain and his courtiers—Peter the Great—His tax upon beards—Revival of beards and moustaches after the French Revolution of 1830—The King of Bavaria (1838) orders all civilians wearing moustaches to be arrested and shaved—Examples from Bayeux tapestry

Preface.

In reading the history of nations, we find that, like individuals, they have their whims and their peculiarities; their seasons of excitement and recklessness, when they care not what they do. We find that whole communities suddenly fix their minds upon one object, and go mad in its pursuit; that millions of people become simultaneously impressed with one delusion, and run after it, till their attention is caught by some new folly more captivating than the first. We see one nation suddenly seized, from its highest to its lowest members, with a fierce desire of military glory; another as suddenly becoming crazed upon a religious scruple; and neither of them recovering its senses until it has shed rivers of blood and sowed a harvest of groans and tears, to be reaped by its posterity. At an early age in the annals of Europe its population lost their wits about the sepulchre of Jesus, and crowded in frenzied multitudes to the Holy Land; another age went mad for fear of the devil, and offered up hundreds of thousands of victims to the delusion of witchcraft. At another time, the many became crazed on the subject of the philosopher’s stone, and committed follies till then unheard of in the pursuit. It was once thought a venial offence, in very many countries of Europe, to destroy an enemy by slow poison. Persons who would have revolted at the idea of stabbing a man to the heart, drugged his pottage without scruple. Ladies of gentle birth and manners caught the contagion of murder, until poisoning, under their auspices, became quite fashionable. Some delusions, though notorious to all the world, have subsisted for ages, flourishing as widely among civilised and polished nations as among the early barbarians with whom they originated,—that of duelling, for instance, and the belief in omens and divination of the future, which seem to defy the progress of knowledge to eradicate them entirely from the popular mind. Money, again, has often been a cause of the delusion of multitudes. Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper. To trace the history of the most prominent of these delusions is the object of the present pages. Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.

Some of the subjects introduced may be familiar to the reader; but the Author hopes that sufficient novelty of detail will be found even in these, to render them acceptable, while they could not be wholly omitted in justice to the subject of which it was proposed to treat. The memoirs of the South-Sea madness and the Mississippi delusion are more complete and copious than are to be found elsewhere; and the same may be said of the history of the Witch Mania, which contains an account of its terrific progress in Germany, a part of the subject which has been left comparatively untouched by Sir Walter Scott in his Letters on Demonology and Witchcraft, the most important that have yet appeared on this fearful but most interesting subject.

Popular delusions began so early, spread so widely, and have lasted so long, that instead of two or three volumes, fifty would scarcely suffice to detail their history. The present may be considered more of a miscellany of delusions than a history—a chapter only in the great and awful book of human folly which yet remains to be written, and which Porson once jestingly said he would write in five hundred volumes! Interspersed are sketches of some lighter matters,—amusing instances of the imitativeness and wrongheadedness of the people, rather than examples of folly and delusion.

Religious matters have been purposely excluded as incompatible with the limits prescribed to the present work; a mere list of them would alone be sufficient to occupy a volume.

April 15th, 2018

A rhetorical question? Genuine concern?

In this essay we are examining another form of matter otherwise known as national literary matters, the three most important of which being the Matter of Rome, Matter of France, and the Matter of England.

Our focus shall be on the Matter of England or Britain.

What we are referring to is the Medieval literature and legends underpinning the history of Brittany to include the Arthurian literature of legendary and heroic King Arthur. In contrast, the Matter of France focuses on the legends of Charlemagne and the Matter of Rome was derived from classical mythology.

French poet Jean Bodel’s La Chansondes Saisnes or Song of the Saxon first described the matters thus:

“Ne sont que III matieres a nul momme atandant, De France et de Bretaigne, et de Rome la grant.”

Not but with three matters no man should attend: Of France, and of Britain and of Rome the grand.”

Medieval literature could be considered an early form of state propaganda, written to ensure the acceptance of future kings by providing them with written history and pedigrees of lineage. With grand myths of conquest and great deeds, heroic figures such as King Arthur became important early role models so as to provide the common people with a set of noble attributes by which to expect, see, and believe in their leaders; chief among these being chivalry, honour, and courage. Along with the legend of King Arthur, this literature introduced us to Brutus of Troy, King Lear and Coel Hen. In much of this literature, fact and fiction become blurred as the written word of historians supplemented the myths. Themes of great conquests, adventure, Christianity, loyalty, and love abound in these tales and so does the lesson of negative consequences should one embark upon a darker path in seeking glory.

Among the notable Medieval(12th & 13th centuries) authors of this literature of matters we find Geoffrey of Monmouth, John Milton, Michael Drayton, Thomas Malory, Geoffrey Chaucer, Gottfried Von Strassburg, Chrétian des Troyes, Nennius, Thomas of Britain, and Talisein from the 6th Century. Shakespeare extended the time frame into the Elizabethan Era.

To learn more about Medieval authors and the works that underpin the Matter of Britain, click here.

February 24th, 2026

National Literary Matters: Matter of Rome, Matter of France, Matter of England

The three “Matters” were first described in the 12th century by French poet Jean Bodel, whose epic La Chanson des Saisnes (“Song of the Saxons”) contains the line:

Ne sont que III matières à nul homme atandant,

De France et de Bretaigne, et de Rome la grant.

“Not but with three matters no man should attend:

Of France, and of Britain, and of Rome the grand.”

The name distinguishes and relates the Matter of Britain from the mythological themes taken from classical antiquity, the “Matter of Rome”, and the tales of the paladins of Charlemagne and their wars with the Moors and Saracens, which constituted the “Matter of France”. Arthur is the chief subject of the Matter of Britain, along with stories related to the legendary kings of the British, as well as lesser-known topics related to the history of Great Britain and Brittany, such as the stories of Brutus of Troy, Coel Hen, Leir of Britain (King Lear), and Gogmagog. Continue reading Matter of Britain

April 11th, 2018

BLACKBERRY WINE

- 5 gallons of blackberries

- 5 pound bag of sugar

Fill a pair of empty five gallon buckets half way with hot soapy water and a ¼ cup of vinegar. Wash thoroughly and rinse.

Fill one bucket with two and one half gallons of blackberries and crush with hickory wood ax handle. Add remaining 2 ½ gallons of berries and crush. Add 2 ½ gallons of well water to berries, cover with muslin cloth and jute twine gardening string. Allow to stand for 24 hours.

Strain through muslin cloth into second bucket.

Add a pound and a half of sugar to each gallon of juice. Cover with muslin cloth and secure with jute twine gardening string. When fermentation process ends, refine through muslin cloth into second bucket, fine with metabisulfate if needed, bottle and cork or store in wooden cask.

April 11th, 2018

A CROCK OF SQUIRREL

- 4 young squirrels – quartered

- Salt & Pepper

- 1 large bunch of fresh coriander

- 2 large cloves of garlic

- 2 tbsp. salted sweet cream cow butter

- ¼ cup of brandy

- 1 tbsp. turbinado sugar

- 6 fresh apricots

- 4 strips of bacon

- 1 large package of Monterrey brown mushrooms

- 2 small red onions quartered and sliced

- ½ cup pecan halves

Grease crock pot with olive oil, turn on high heat. Cover bottom with 1 small red onion. Fry bacon in skillet coated with olive oil along with 1 small red onion quartered and sliced and 2 clove smashed and chopped garlic. As bacon begins to cook cut each piece in skillet into 6-8 pieces. Add mushrooms as bacon begins to firm.

Remove pits from 6 fresh apricots and quarter. Sauté in butter and brandy till wilted. Add pecans and sugar. Stir over medium heat for a couple of minutes. In large mixing bowl, combine with bacon mixture, add fresh chopped coriander & coat squirrels. Cook for 4 hours on low heat. Serve with biscuits and creamed corn.

April 11th, 2018 FRIED SQUIRREL & BISCUIT GRAVY

- 3-4 Young Squirrels, dressed and cleaned

- 1 tsp. Morton Salt or to taste

- 1 tsp. McCormick Black Pepper or to taste

- 1 Cup Martha White All Purpose Flour

- 1 Cup Hog Lard – Preferably fresh from hog killing, or barbecue table

Cut up three to four young squirrels into six pieces by using a meat cleaver and splitting the squirrel down the center of the backbone prior to cutting into sections. Continue reading A Couple of Classic Tennessee Squirrel Recipes

April 8th, 2018

THE FOWLING PIECE, from the Shooter’s Guide by B. Thomas – 1811.

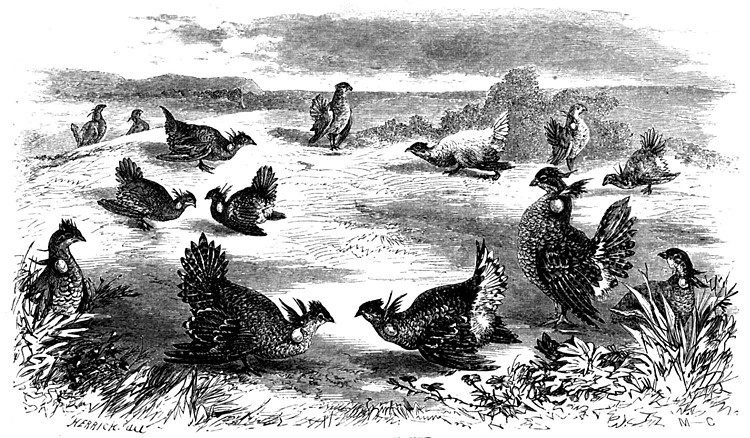

I AM perfectly aware that a large volume might be written on this subject; but, as my intention is to give only such information and instruction as is necessary for the sportsman, I shall forbear introducing any extraneous matter; at the same time, being careful to omit nothing which can be useful even in the remotest degree. That the fowling-piece is an object of the first consideration, will be readily allowed; hence the necessity of being able to form an opinion of its merits prior to laying out a considerable sum of money on this article, as Well as to prevent those dreadful accidents which too frequently occur from causes which at first sight are by no means obvious. Continue reading The Fowling Piece – Part I

April 7th, 2018

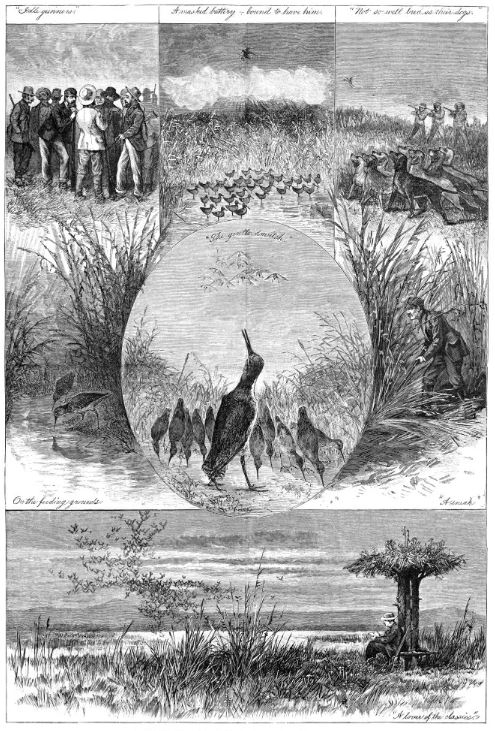

THE SNIPE, from the Shooter’s Guide by B. Thomas – 1811

AFTER having given a particular description of the woodcock, it will only. be necessary to observe, that the plumage and shape of the snipe is much the same ; and indeed its habits and manners sets bear a great analogy. But there are three different sizes of snipes, the largest of which, however, is much smaller than the woodcock. The common snipe, weighs about four ounces, the jack snipe. is not much. bigger than a lark; the large snipe weighs about nine ounces, but is seldom met with. Some have supposed that the common snipe is the jack’s female ; however, the contrary is now too well known to need a refutation in this place. Continue reading The Snipe

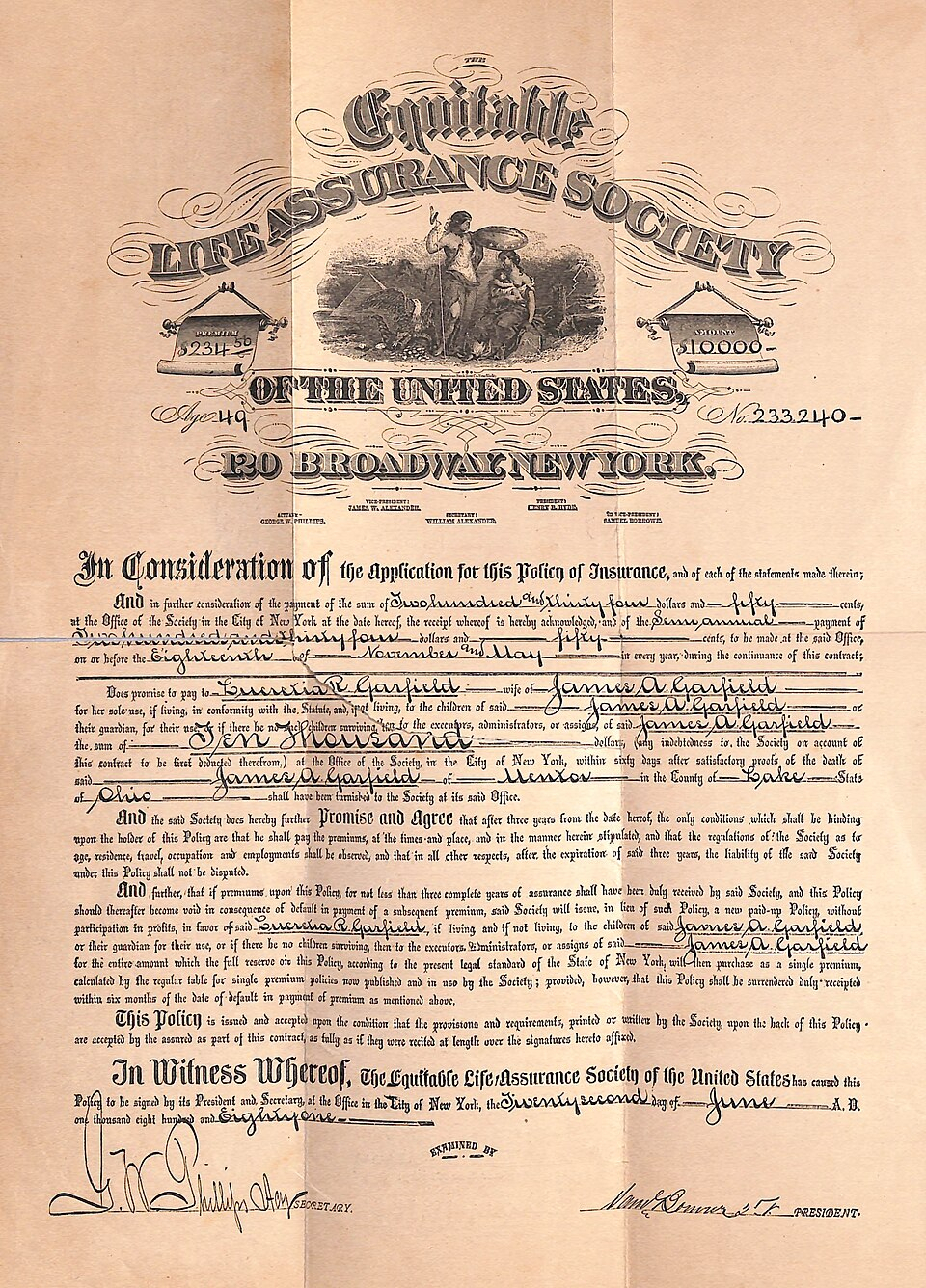

February 24th, 2026  A $10,000 life insurance policy written by the Equitable Life Assurance Society of the United States for President James A. Garfield. It was signed on the 22nd of June, 1881, 9 days before President Garfield was shot by Charles J. Guiteau on July 2. From How to Make Money; and How to Keep it, Or, Capital and Labor based on the works of Thomas A. Davies Revised & Rewritten with Additions by Henry A. Ford A.M.

CHAPTER XXVII.

LIFE INSURANCE.

It is an unselfish, generous act when one takes out a life policy to protect his family. Not only this, but he is doing his simple duty. ANONYMOUS.

The Life Insurance system has been for two centuries a positive force in the progress of modern civilization and the accumulation of national wealth. It has been an important educational factor in every community, which it has influenced in habits of economy, prudence, and providence. And it stands to-day side by side with the savings-bank and the trust company, sharing the confidence with which men who seek the welfare of their fellows crown all three. Rev. STEPHEN H. TYNG Jr.

THE origin of life insurance is attributed to the Rev. Wm. Anhote, D. D., of Middleton, Lancashire, England, who opened a public office about two hundred years ago, for the benefit of widows, especially those of clergy men, and for the settling of jointures and annuities. In 1698, the “Mercers’ Company” began to assure lives for the benefit of widows; and in July, 1806, under charter from Queen Anne, the “Amicable Society, or Perpetual Assurance,” opened the first general office. Within a century and a half from that time, about one hundred life companies were founded in the United Kingdom. In 1820 the ” Hospital Life Insurance Company,” first in this country, began its operations in Boston. Twenty-three years afterwards the first mutual companies were founded in that city and in New York. The number of life companies in the United States is now very large, and the system of late years has had an enormous development. It has become a highly important feature in the financial world; and its object is of a nature likely to commend it to every thinking mind. We have before insisted that it is the moral and political duty of every one so to arrange his affairs that he shall under no circumstances become a burden upon the public or his friends: we now say that this branch of finance offers the best way in which such result can be obtained. For if the man be alone in the world, with no one dependent upon him, it can be shown that he will accumulate for himself as fast in some other way on small amounts, while if he has others dependent upon him, this is the only way by which an independence can certainly be assured to them.

However industrious, prudent, and saving one may be under circumstances that protect him and his, Death stands at his door to put an end at any time to such efforts, however well directed. From the responsibilities of this end there is but one loophole of escape, but one way by which the man thus situated may see his way clear, and conquer even the efforts of Death to thwart him. Life insurance meets the case; and while it does this effectually, if at the same time it accomplishes the further end of causing money to make money to the best advantage, it is still better. But if, again, it shows how to do this, and also to keep the accumulations, a treble triumph is won; and three problems harder to solve are not found in the whole range of finance. If, then, their solution can be accomplished by the most simple and untrained of financiers, this may be said to be the El Dorado of the protector’s hope, if not of the unskilled money-maker and hoarder of his gains.

Let anyone, then, who has such obligations upon him, consider well their binding force, politically and socially, even if he have no promptings of love or gratitude to the same end. As an anonymous writer has put it, “What a neglect of duty it is for a head of a house to go uninsured! Probably more than two-thirds of the families in any community are dependent for their subsistence upon the daily earnings of the husband or father. Precarious, indeed, must that subsistence be, which hangs wholly and absolutely upon one life–that of the father. When he ceases to exist, not only a parent dies, but a fortune perishes. Then is his life-the mint-closed to those who drew from it. How deplorable such a state of things must be when so many sudden deaths occur ! “

Let the husband and father look over the following mortality table, and see what his expectancy of life is. It will in all probability arouse him to sudden and energetic action in the right direction, before his opportunities are past with no chance to retrace or amend his ways.

|

|

|

![50 Watt 4 Stage Hi-Fidelity Power Amplifier Circuit and Parts List [The Basic Schematic of Most Low Cost Tube Guitar Amps Made Today]](https://countryhouseessays.com/wp-content/uploads/2026/02/5R4GYB-Tube.gif)