![50 Watt 4 Stage Hi-Fidelity Power Amplifier Circuit and Parts List [The Basic Schematic of Most Low Cost Tube Guitar Amps Made Today]](https://countryhouseessays.com/wp-content/uploads/2026/02/5R4GYB-Tube.gif)

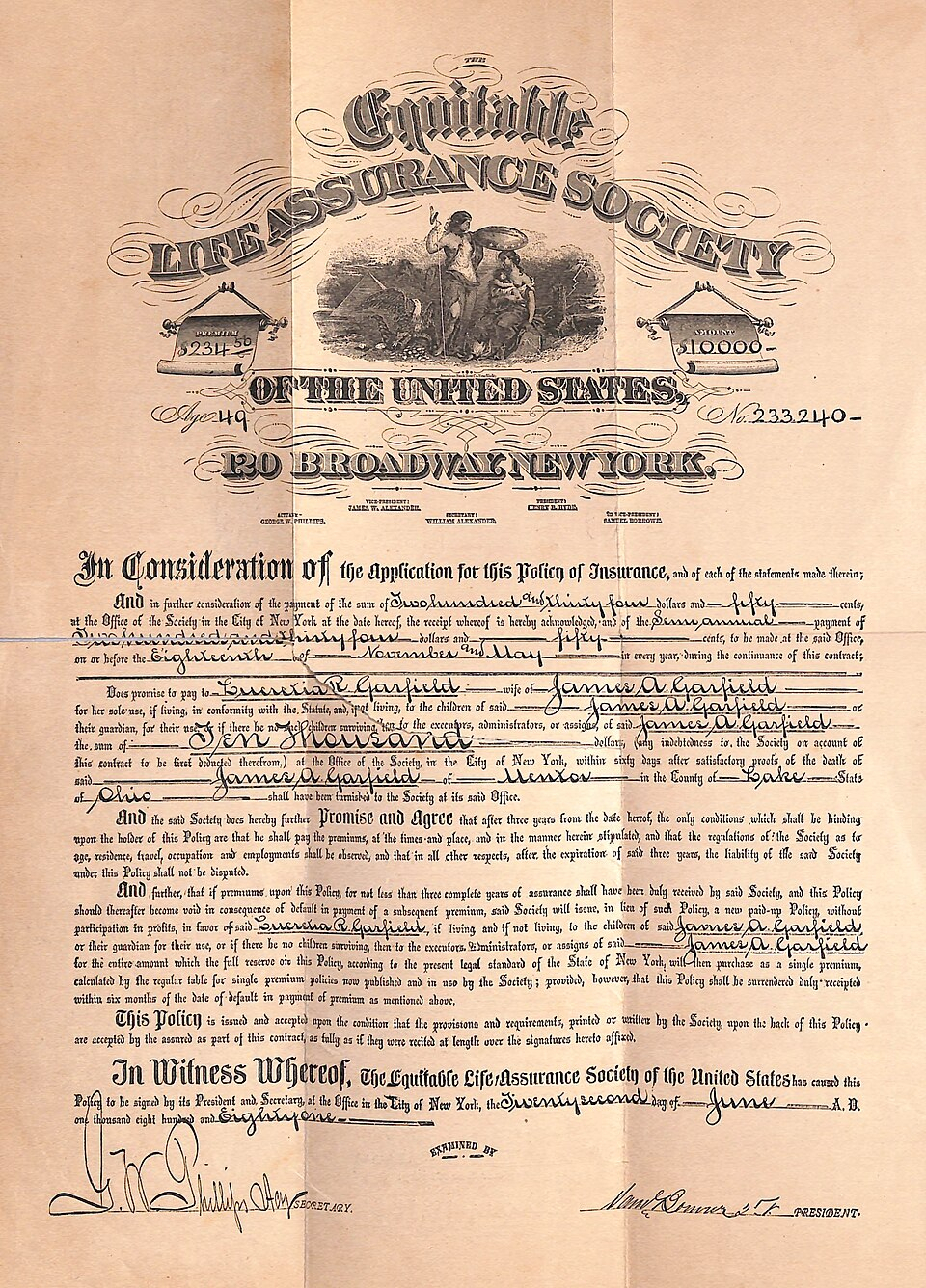

A $10,000 life insurance policy written by the Equitable Life Assurance Society of the United States for President James A. Garfield. It was signed on the 22nd of June, 1881, 9 days before President Garfield was shot by Charles J. Guiteau on July 2.

From How to Make Money; and How to Keep it, Or, Capital and Labor based on the works of Thomas A. Davies Revised & Rewritten with Additions by Henry A. Ford A.M.

CHAPTER XXVII.

LIFE INSURANCE.

It is an unselfish, generous act when one takes out a life policy to protect his family. Not only this, but he is doing his simple duty. ANONYMOUS.

The Life Insurance system has been for two centuries a positive force in the progress of modern civilization and the accumulation of national wealth. It has been an important educational factor in every community, which it has influenced in habits of economy, prudence, and providence. And it stands to-day side by side with the savings-bank and the trust company, sharing the confidence with which men who seek the welfare of their fellows crown all three. Rev. STEPHEN H. TYNG Jr.

THE origin of life insurance is attributed to the Rev. Wm. Anhote, D. D., of Middleton, Lancashire, England, who opened a public office about two hundred years ago, for the benefit of widows, especially those of clergy men, and for the settling of jointures and annuities. In 1698, the “Mercers’ Company” began to assure lives for the benefit of widows; and in July, 1806, under charter from Queen Anne, the “Amicable Society, or Perpetual Assurance,” opened the first general office. Within a century and a half from that time, about one hundred life companies were founded in the United Kingdom. In 1820 the ” Hospital Life Insurance Company,” first in this country, began its operations in Boston. Twenty-three years afterwards the first mutual companies were founded in that city and in New York. The number of life companies in the United States is now very large, and the system of late years has had an enormous development. It has become a highly important feature in the financial world; and its object is of a nature likely to commend it to every thinking mind. We have before insisted that it is the moral and political duty of every one so to arrange his affairs that he shall under no circumstances become a burden upon the public or his friends: we now say that this branch of finance offers the best way in which such result can be obtained. For if the man be alone in the world, with no one dependent upon him, it can be shown that he will accumulate for himself as fast in some other way on small amounts, while if he has others dependent upon him, this is the only way by which an independence can certainly be assured to them.

However industrious, prudent, and saving one may be under circumstances that protect him and his, Death stands at his door to put an end at any time to such efforts, however well directed. From the responsibilities of this end there is but one loophole of escape, but one way by which the man thus situated may see his way clear, and conquer even the efforts of Death to thwart him. Life insurance meets the case; and while it does this effectually, if at the same time it accomplishes the further end of causing money to make money to the best advantage, it is still better. But if, again, it shows how to do this, and also to keep the accumulations, a treble triumph is won; and three problems harder to solve are not found in the whole range of finance. If, then, their solution can be accomplished by the most simple and untrained of financiers, this may be said to be the El Dorado of the protector’s hope, if not of the unskilled money-maker and hoarder of his gains.

Let anyone, then, who has such obligations upon him, consider well their binding force, politically and socially, even if he have no promptings of love or gratitude to the same end. As an anonymous writer has put it, “What a neglect of duty it is for a head of a house to go uninsured! Probably more than two-thirds of the families in any community are dependent for their subsistence upon the daily earnings of the husband or father. Precarious, indeed, must that subsistence be, which hangs wholly and absolutely upon one life–that of the father. When he ceases to exist, not only a parent dies, but a fortune perishes. Then is his life-the mint-closed to those who drew from it. How deplorable such a state of things must be when so many sudden deaths occur ! “

Let the husband and father look over the following mortality table, and see what his expectancy of life is. It will in all probability arouse him to sudden and energetic action in the right direction, before his opportunities are past with no chance to retrace or amend his ways.